In this blog, CSG is summarizing three key aspects that support the Medicare market’s growth opportunities to carriers, marketing organizations and agents. First, the demographic tailwinds evidenced by the continued growth in enrollments by market leaders. Second, there continues to be acquisition activity in the Senior market marketing organization space. CSG provides a listing of transactions announced year-to-date. Lastly, significant profits are being reported by the large public-company carriers due to lower utilization. CSG looks at the medical benefit ratios from key carriers as reported in their 2nd Quarter 2020 financials.

Demographic Tailwinds & Enrollment Growth from market leaders

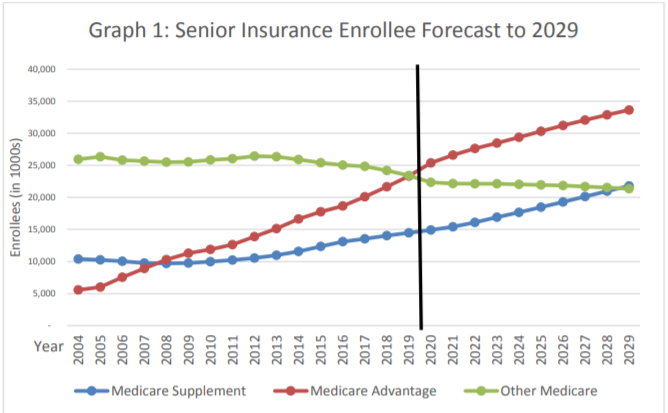

Over 76 million individuals are expected to be enrolled in the Medicare program by 2029. This means that roughly 15 million more individuals will be added to the Medicare program over the next 10 years, a 25% increase. Source: CSG Actuarial 10th Annual Medicare Supplement Market Projection.

Strong enrollment growth from the Medicare market leaders:

CSG previously reported Medicare Supplement market leader United Healthcare’s (UHC) strong growth in adding 10,000 Medicare Supplement lives in the Q2 2020.

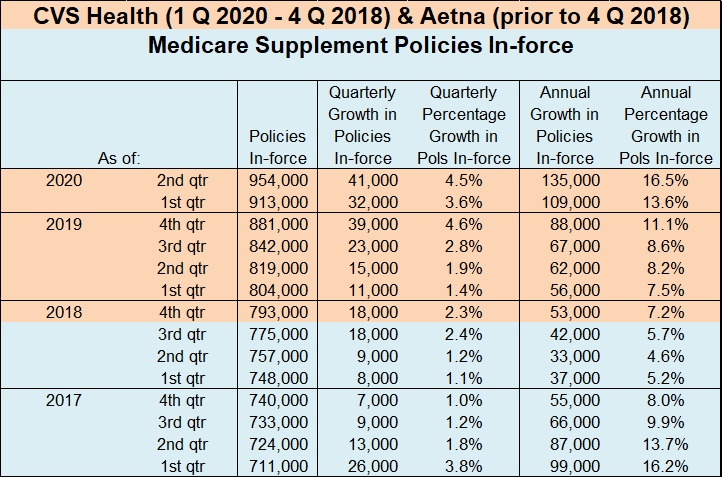

CVS Health Medicare Supplement Enrollment Increases 41,000 during the Q2 2020.

CVS Health recently reported Q2 2020 results with Medicare Supplement member in-force counts of 954,000, up 73,000 from 4th quarter 2019 and 135,000 over the past 12 months.

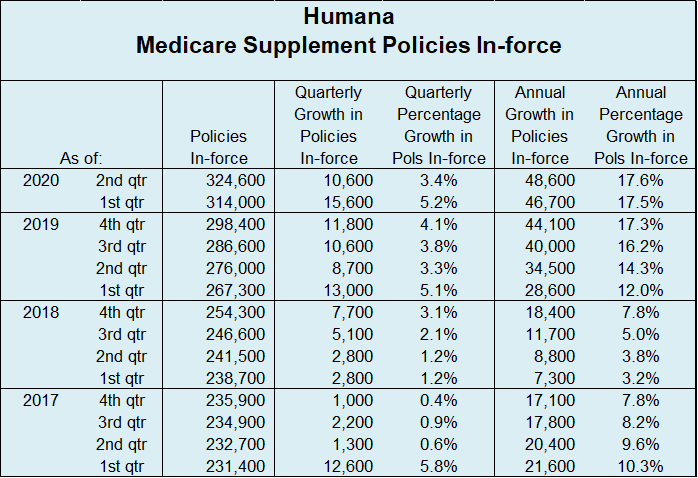

Humana Medicare Supplement Enrollment Increases 10,600 in 2nd Quarter 2020

Humana reported 2nd Quarter 2020 Medicare Supplement lives of 324,600, up 26,200 from 4th quarter 2019 and a 48,600 increase over 2nd quarter 2019.

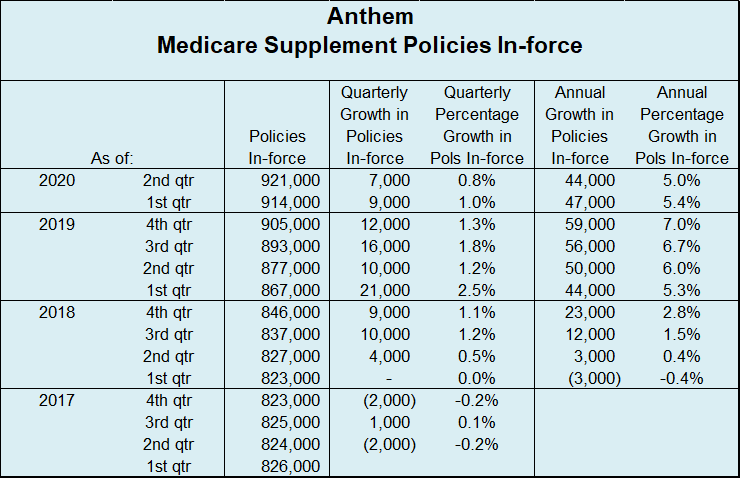

Anthem Medicare Supplement Enrollment Increases 7,000 during 2nd Quarter 2020

Anthem, Inc. added 7,000 Medicare Supplement lives in the 2nd quarter and 44,000 Medicare Supplement lives in the past 12 months.

Acquisitions in the Senior Market FMO/IMO Space

COVID related shutdowns and travel restrictions have not slowed M&A activity with marketing organizations in the Senior space. CSG has compiled a table summarizing acquisitions year-to-date in 2020 in the Medicare space. For additional information on each transaction, click on the hyper-link to review the press release for each transaction.

| Date Announced | Target Company | Acquirer |

|---|---|---|

| 1/7/2020 | Stephens-Mathews Marketing Inc. | Amerilife |

| 1/28/2020 | Agent Pipeline, Inc. | Integrity Marketing Group |

| 2/12/2020 | J.D.Mellberg Financial | Amerlife |

| 2/25/2020 | Palmetto Senior Benefits | Integrity Marketing Group |

| 3/3/2020 | Taylor Financial & Insurance Services ("FFL USA") | Integrity Marketing Group |

| 3/10/2020 | LifeSmart Senior Services, Inc. | Integrity Marketing Group |

| 3/19/2020 | Killimett Agency ("FFL Southeast") | Integrity Marketing Group |

| 4/1/2020 | Jack Schroeder & Associates, Inc. | Amerilife |

| 4/14/2020 | The Brokerage Resource, Inc. | Integrity Marketing Group |

| 4/19/2020 | Equis Financial, Inc. | Integrity Marketing Group |

| 5/19/2020 | Pinnacle Financial Services | Amerilife |

| 6/2/2020 | Tri-State Financial | Integrity Marketing Group |

| 6/15/2020 | Formula Folios, Inc. | Amerilife |

| 6/18/2020 | McNerney Management Group | Integrity Marketing Group |

| 6/30/2020 | National Agents Alliance ("The Alliance") | Integrity Marketing Group |

| 7/13/2020 | Benefytt Technologies, Inc. (formerly Health Insurance Innovations) | Madison Dearborn Partners |

| 7/14/2020 | McClain Insurance | Integrity Marketing Group |

| 7/21/2020 | New Horizons Insurance Marketing | Integrity Marketing Group |

| 7/29/2020 | Senior Market Sales, Inc. | Alliant |

| 8/4/2020 | Heartland Retirement Group | Integrity Marketing Group |

| 8/4/2020 | Agent Force | Integrity Marketing Group |

| 8/4/2020 | Crosspointe Insurance Advisors | EverQuote |

| 8/13/2020 | ASB Financial | Integrity Marketing Group |

| 8/18/2020 | Southern Insurance Group | Integrity Marketing Group |

CSG previously reported on the successful IPOs of SelectQuote, Inc and GoHealth, Inc that raised a combined $1.3 billion.

Significant reduction in Medical Loss Ratios

The table below shows the significantly lower medical loss ratios reported by several public company Health Insurance carriers for Q2 2020. The lower utilization is obviously a result of the pandemic stay-at-home orders.

Public Company Health Carriers

| Medical Benefit Ratio Comparison | |||||

|---|---|---|---|---|---|

| Source: Company 10Q | |||||

| Three months ended June 30 | Six months ended June 30 | ||||

| Company | Reportable Segment | 2020 | 2019 | 2020 | 2019 |

| CVS Health | Health Benefit Segment | 70.3% | 84.0% | 76.4% | 84.0% |

| United Health Group | UnitedHealthcare | 70.2% | 83.1% | 75.75 | 82.5% |

| Humana | Retail Segment | 78.3% | 85.2% | 82.4% | 86.7% |

| Cigna | Integrated Medical Segment | 70.5% | 81.6% | 74.5% | 80.3% |

| Anthem | Consolidated Operations | 77.9% | 86.7% | 81.1% | 85.6% |

| Centene | Consolidated Operations | 82.1% | 86.7% | 84.9% | 86.2% |

Many carriers implemented programs to support their Medicare members during the pandemic such as waiving cost-sharing on primary care and tele-health and COVID-19 related services. Americas Health Insurance Plans (“AHIP”) maintains a thorough summary of health insurance carrier responses to the COVID-19 pandemic.

What does it mean to you?

Whether you represent a carrier, a field marketing organization, agency or you’re an agent serving the needs of your community, CSG Actuarial provides a variety of services such as Actuarial Consulting Product Development, Compliance Services for carriers looking to enter the market.

Reach out to us to learn more about our consulting services, software quoting and e-app solutions, or have interest in our other market projections on the Senior Dental, Senior HIP, Final Expense, Short-term Care, Accident and Critical Illness markets.

Questions? Contact:

Jason Yoo, Director of Market Research; jyoo@csgactuarial.com; 855-861-8776 x103